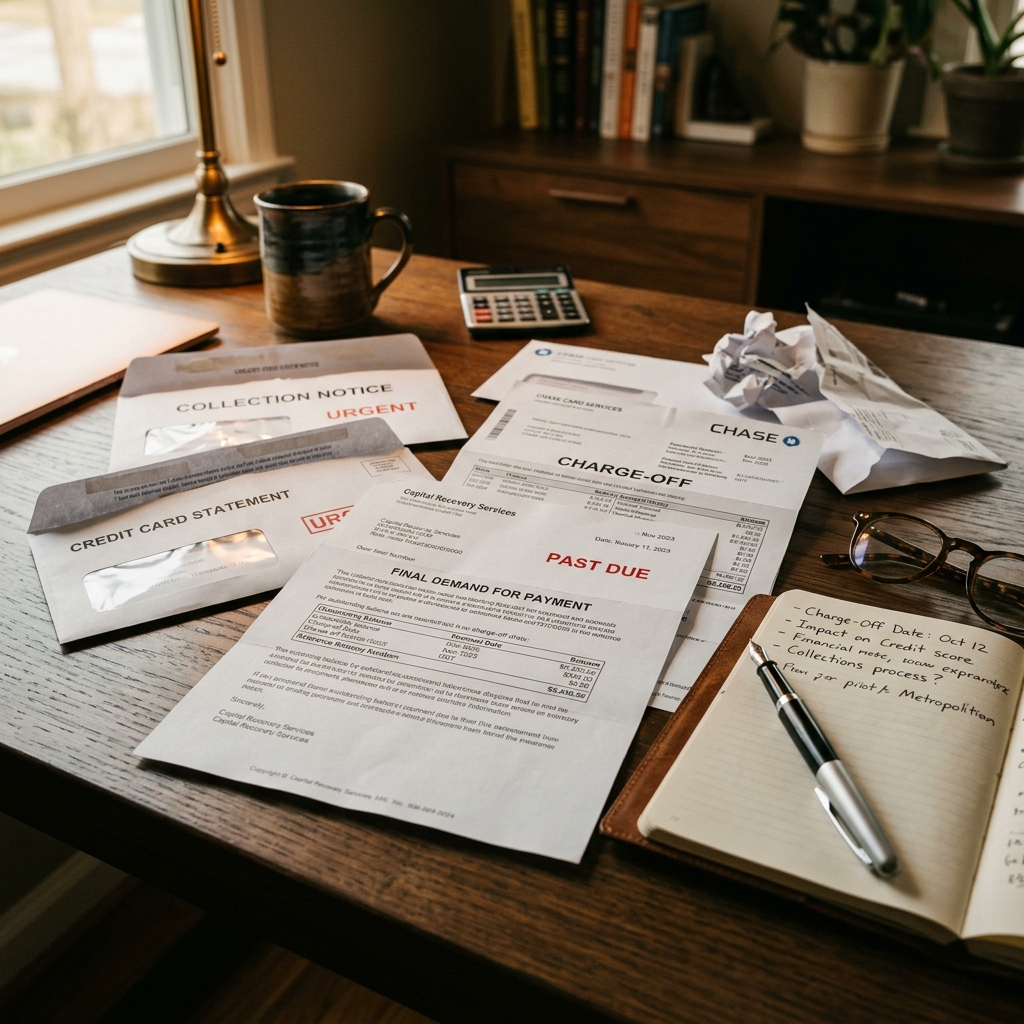

A charge off sounds like the debt disappeared. It did not. A charge off is an accounting move by the creditor, usually after several months of missed payments. The creditor is saying they do not expect to collect the account as agreed.

That does not mean you no longer owe the money. It also does not mean collection activity has to stop.

What a charge off means

When an account charges off, the original creditor may keep trying to collect, assign it to a collection agency, sell it to a debt buyer, or eventually consider legal action.

The account may show on your credit reports as charged off with a past-due balance. If it is sold to a debt buyer, you may also see a separate collection account.

That double reporting can feel unfair, but it is common. The key is checking whether the balances, dates, and ownership details are accurate.

What can happen next

After a charge off, you may receive calls, letters, settlement offers, or notices from collection agencies. Some accounts sit quietly for a while and then resurface later.

If a collector contacts you, pay attention to deadlines. You may have the right to request validation of the debt. If you receive court papers, read them carefully and speak with a qualified attorney.

Missing a court deadline can lead to a default judgment, so it is worth getting guidance early.

Can you settle a charged-off account?

Sometimes, yes. Charged-off accounts are often candidates for settlement because the creditor or debt buyer may be willing to accept less than the full balance.

But there are no guarantees. The amount depends on who owns the account, how old it is, your hardship, the available funds, and the collector’s policies.

Before paying, get the settlement terms in writing. Keep proof of payment and any final letter showing the account was resolved.

How long does it stay on credit reports?

A charge off can generally remain on a credit report for up to seven years from the date the account first became delinquent and was never brought current. Paying or settling does not usually erase that history.

That said, a resolved balance may still be better than an unpaid one when future lenders manually review your file.

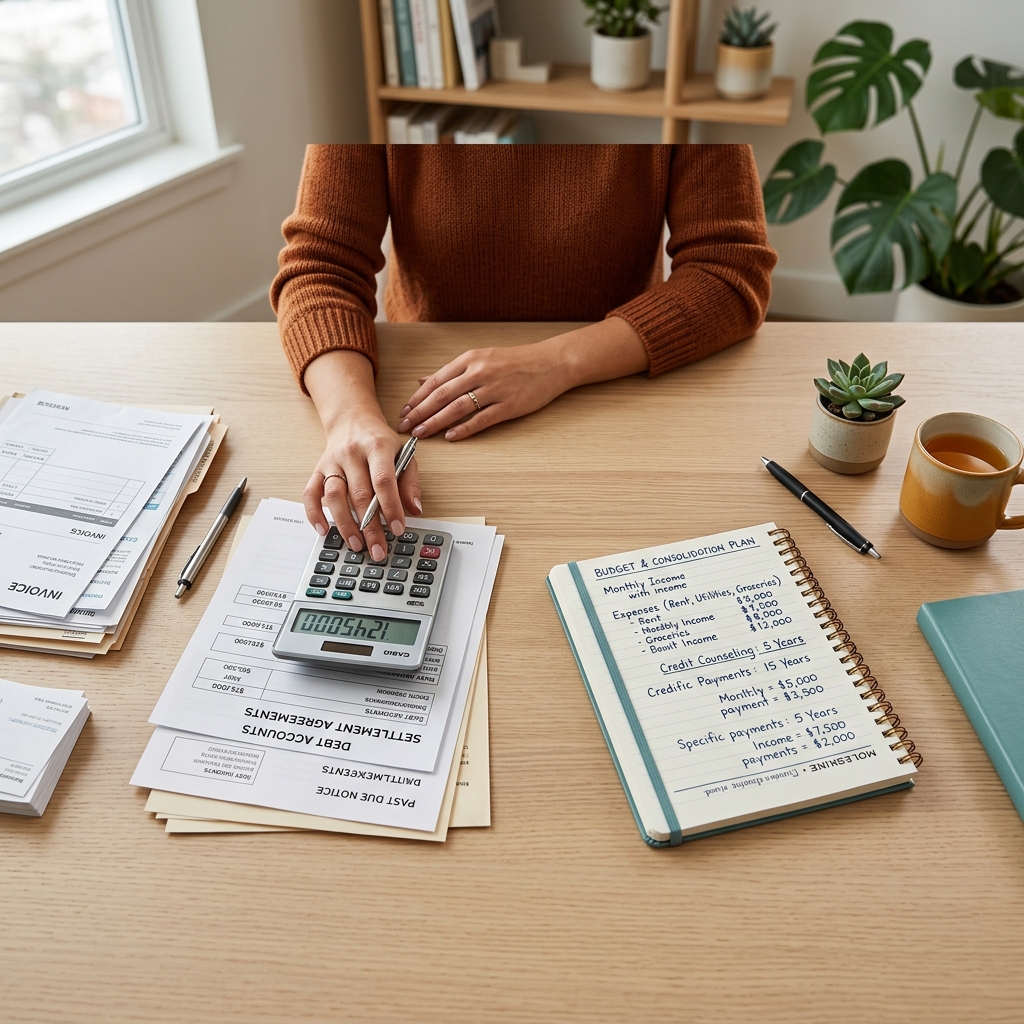

What to do first

Pull your credit reports, list who owns each account, compare balances, and separate accounts that are only reporting from accounts actively collecting.

Then decide whether you are trying to settle, dispute inaccurate information, talk to a bankruptcy attorney, or use another debt relief path. If you need help comparing the routes, start with the debt settlement overview or share your situation through the options form.