Debt settlement and bankruptcy are both serious debt relief options, but they solve different problems. The right question is not which one sounds better. The better question is which one fits your income, assets, account status, goals, and comfort level.

If you are comparing these choices, your regular payments may no longer fit. You may be behind, close to falling behind, or trying to understand collection accounts.

What debt settlement tries to do

Debt settlement is an attempt to resolve unsecured debt for less than the full balance. It is most commonly discussed with credit cards, personal loans, medical bills, and collection accounts.

The basic idea is that a creditor or debt buyer may accept a reduced amount when they believe full repayment is unlikely. That can happen through a lump sum or short payment arrangement.

Settlement is not guaranteed. Some creditors negotiate. Some do not. Some accounts settle only after they are delinquent or charged off. That is why settlement can affect credit, collections, taxes, and legal risk.

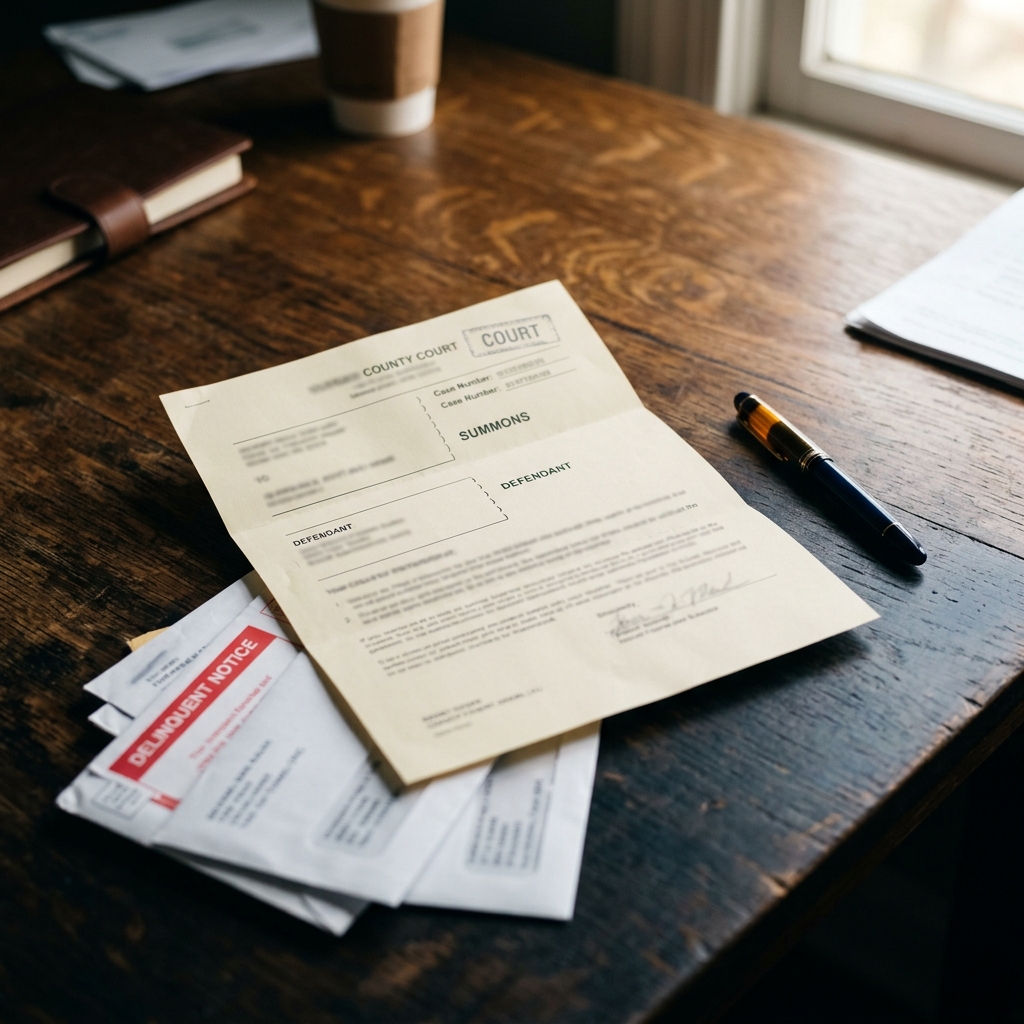

What bankruptcy tries to do

Bankruptcy is a legal process handled through federal court. It can discharge or reorganize certain debts, depending on the chapter and your eligibility.

Chapter 7 can wipe out many unsecured debts for people who qualify. Chapter 13 creates a court supervised repayment plan that usually lasts three to five years.

Bankruptcy can be emotionally hard to consider, but it may offer stronger legal protection than settlement in some situations.

When settlement may fit

Debt settlement may be worth learning about if you have unsecured debt, cannot keep up with payments, want to avoid bankruptcy if possible, and have a way to fund offers over time.

It may also make sense when the total debt is significant but still small enough that realistic settlement funds could resolve it. The math matters. Settlement usually depends on having funds available for offers.

Read the full debt settlement guide before assuming it is the cleanest path.

When bankruptcy may fit

Bankruptcy may be worth discussing with an attorney if your debt load is more than your budget can handle, you have legal papers, your wages are at risk, or you need legal protection from creditors.

It can also be the more direct option when debt settlement would take too long or leave too many open questions.

Bankruptcy has consequences, including credit impact and court requirements, but for some people it is the most realistic reset.

Credit impact is not the only issue

People often ask which option is worse for credit. That is understandable, but credit score should not be the only factor.

You also need to consider lawsuits, taxes on forgiven debt, monthly cash flow, emotional stress, job or housing concerns, and how long it will take to get stable again.

Sometimes protecting your income and creating a steady plan matters more than focusing only on a score that is already affected by missed payments.

A practical way to compare

Start with four questions:

- Are you current, behind, charged off, or already in collections?

- Do you have money available to fund settlement offers?

- Do you have legal papers, a judgment, garnishment, or bank levy?

- Would a lower payment plan solve the problem, or is the debt too far beyond your income?

If you are unsure, use the contact form to outline the basics and compare options. A good debt relief conversation should include the risks, not just the selling points.