Sometimes you can settle a debt before a lawsuit. Sometimes you cannot. The difficult part is that you may not know exactly when a creditor or debt buyer plans to file.

That is why timing, documentation, and realistic offers matter.

Why lawsuits happen

Creditors and debt buyers may file a lawsuit when they believe collection calls and letters are not enough. Lawsuits are more common when balances are high, the account is within the statute of limitations, and the collector believes there is a path to payment.

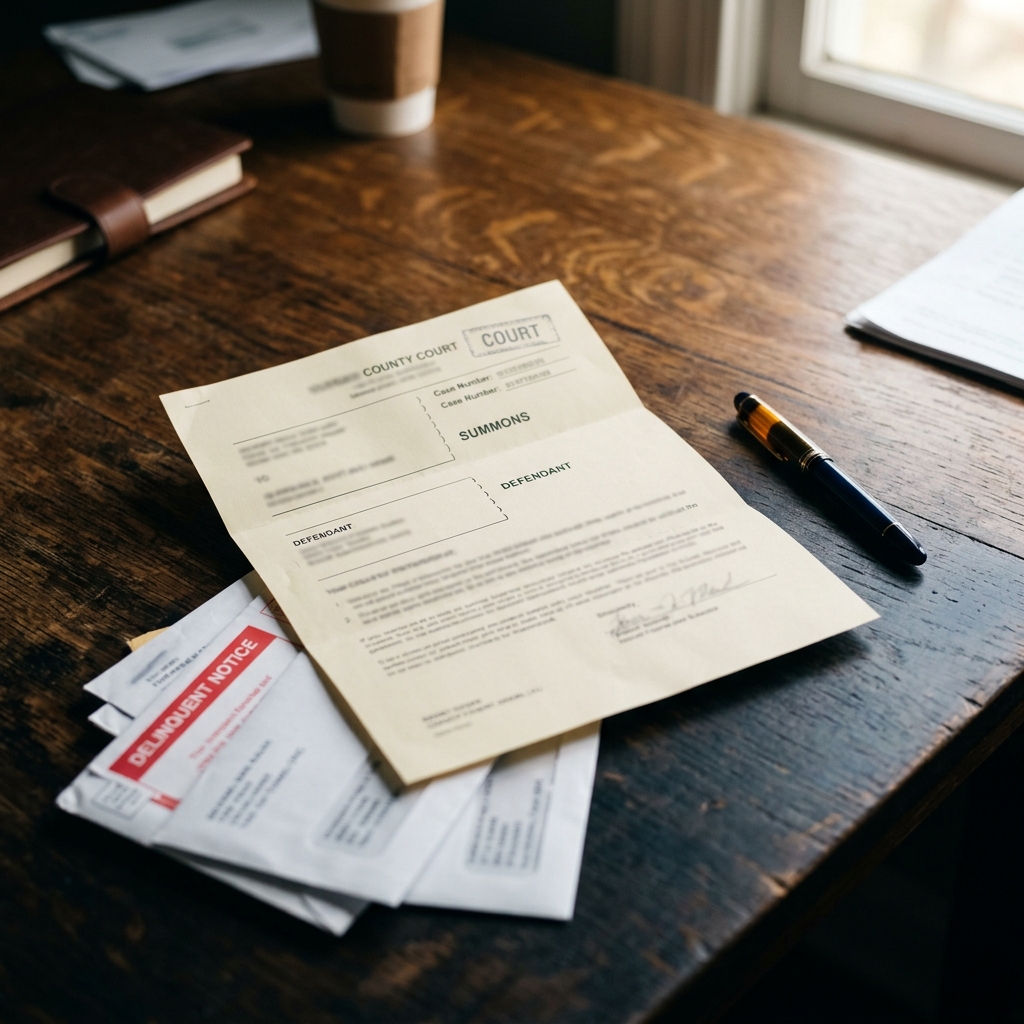

Not every collection account becomes a lawsuit. But if you receive a summons or complaint, the situation has changed. Read the papers carefully and speak with a qualified attorney about the deadline.

Settlement before court papers

Before a lawsuit is filed, settlement may be simpler because there are no court deadlines yet. A collector may accept a lump sum or structured settlement, depending on the account and available funds.

The offer needs to be realistic. A very low offer with no proof of hardship or no ability to pay may not move the conversation.

Always get the agreement in writing before sending money. The letter should identify the account, amount accepted, due date, and what happens after payment.

Settlement after a lawsuit starts

Settlement can still happen after a lawsuit is filed, but there may be court deadlines. Missing those deadlines can lead to a default judgment.

If you receive legal papers, talk to a qualified attorney. Even if you want to settle, you need to understand the court timeline and whether you have defenses.

Do not assume that negotiating on the phone pauses a court case. Get legal guidance and written confirmation.

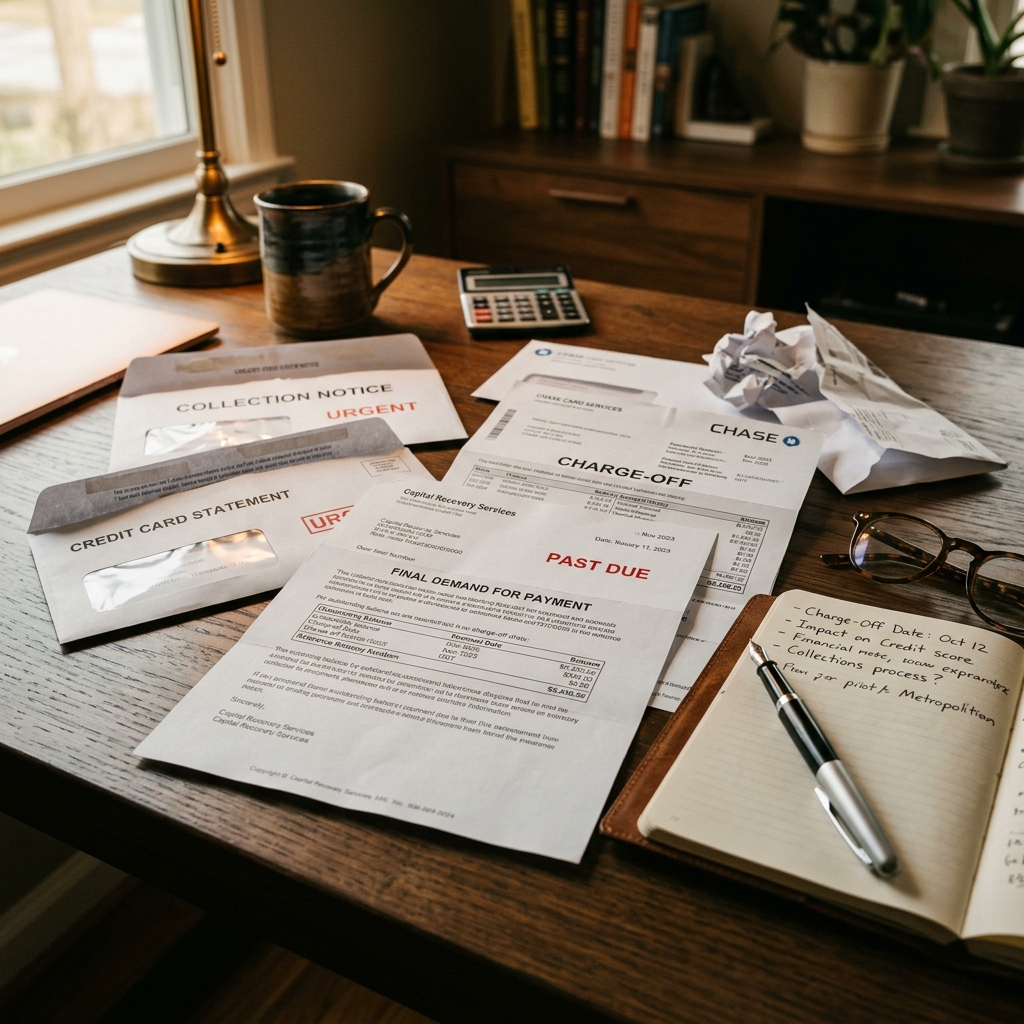

Warning signs to take seriously

Collection letters from law firms, high balances, old accounts approaching limitation deadlines, and repeated settlement deadlines can all be signs to pay closer attention.

That does not mean a lawsuit is guaranteed. It means you should get organized.

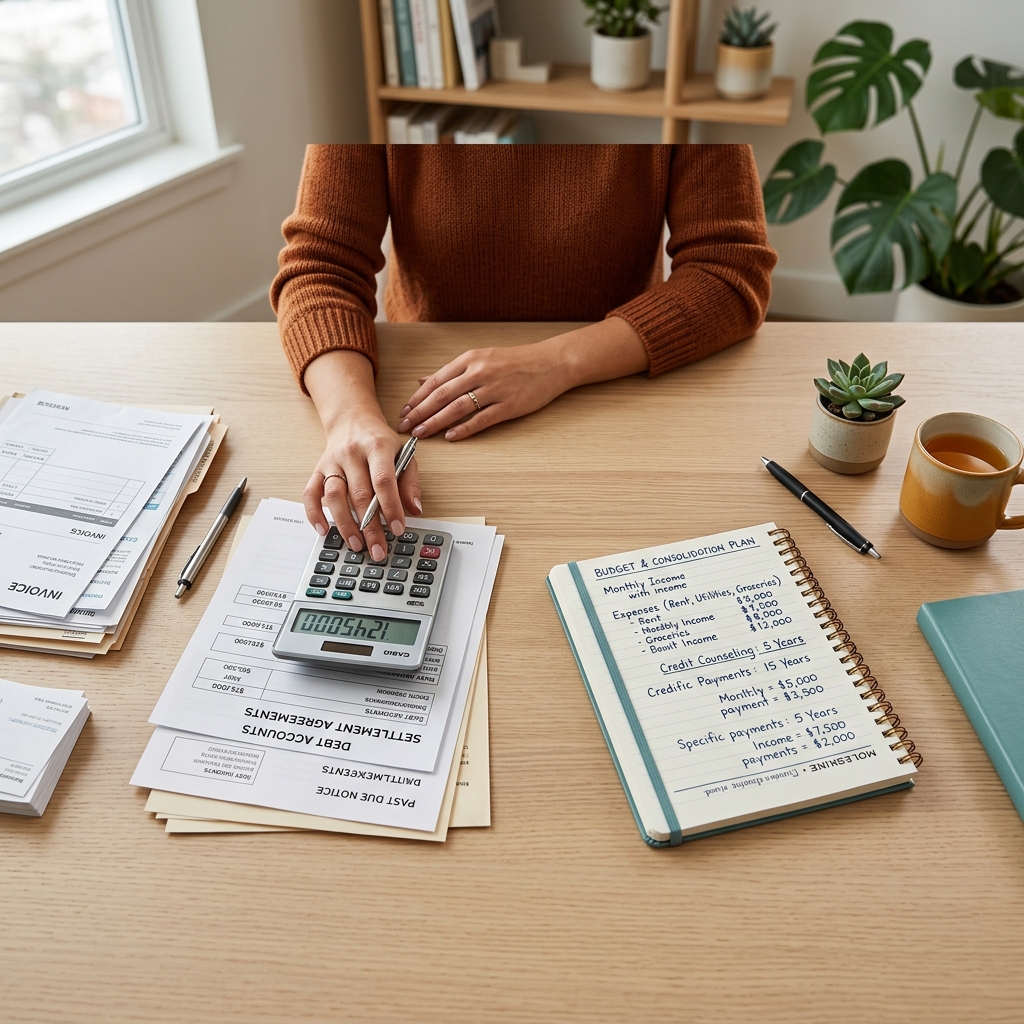

What to gather before negotiating

Collect the creditor name, account number, current collector, balance, last payment date, charge off date, and any letters you received. Also know what money you can actually offer without missing rent, food, utilities, or other essentials.

If you cannot fund a settlement, compare other paths. Bankruptcy information, nonprofit credit counseling, or a different hardship strategy may be more realistic.

For a broader overview, read the debt settlement guide and the article on what happens after a charge off.